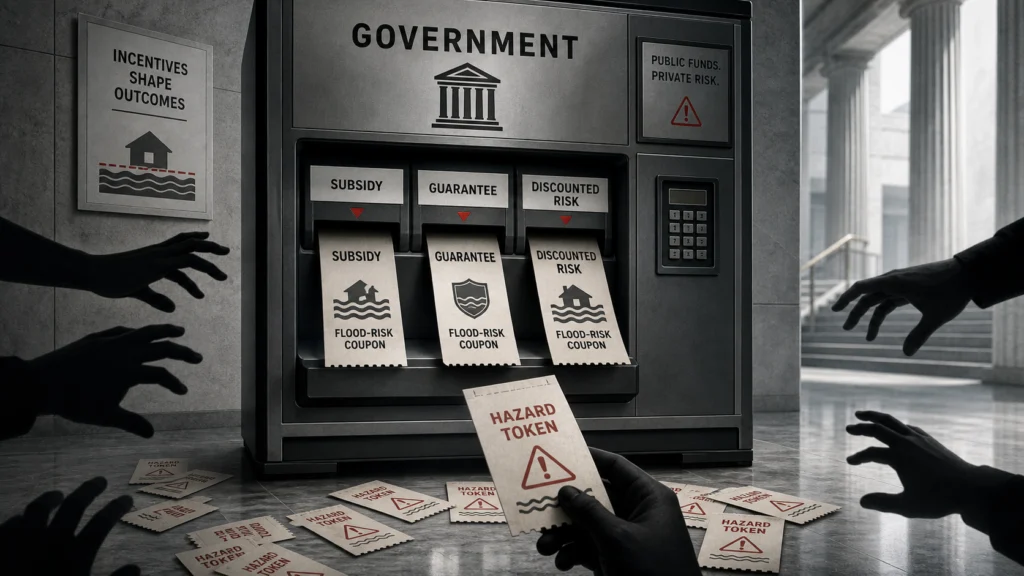

Perverse incentives are what happen when the public goal and the public reward point in opposite directions. A government says it wants less risk, less pollution, or more discipline, then makes risk, pollution, or indiscipline cheaper. The International Monetary Fund’s 2025 update put 2024 fossil fuel subsidies at about $7.4 trillion: $725 billion in explicit subsidies and $6.7 trillion in implicit subsidies, primarily from underpricing environmental costs[s]. That is the pattern: the rulebook condemns one behavior while the budget rewards it.

The one who signs the checks wanted this argument put plainly, which is fair: public systems keep buying yesterday’s quiet and billing tomorrow’s damage.

The mistake is treating perverse incentives as a scandal of motives. Bad motives exist, but they are not required. A policy can be staffed by competent people, defended by sincere officials, and still train citizens, banks, firms, and local governments to do the opposite of what the public says it wants. That is a systems thinking problem, not a character puzzle.

Perverse Incentives Start With Cheap Risk

Flood insurance is the cleanest example because the contradiction is not hidden. The Government Accountability Office says the National Flood Insurance Program has been strained by two competing goals: keeping flood insurance affordable and keeping the program fiscally solvent. GAO also says affordability has led to premium rates that often do not reflect the full risk of loss and do not produce enough premium revenue to pay claims[s].

That is not a small accounting quirk. GAO says this design has shifted some of the financial burden of flood risk from individual property owners to the public at large, and that the program has been on GAO’s High-Risk List since 2006. It also reported that, as of August 2020, FEMA’s debt was $20.5 billion even after Congress canceled $16 billion in debt in October 2017[s].

The perverse incentives here are not that people enjoy danger. They are that the price signal is softened where the risk signal needs to be sharp. If insurance masks the cost of rebuilding in places where losses are likely, then the public has not solved affordability. It has moved part of the bill to people who did not choose the risk.

Guarantees Can Protect People And Reward Recklessness

Bank guarantees show the same tension in a different costume. The Federal Deposit Insurance Corporation says deposit insurance can create moral hazard and increase bank risk-taking, defining moral hazard as the incentive to take greater risk because someone is protected from the consequences of risk-taking[s]. That is a blunt admission from the institution responsible for making deposit insurance work.

Deposit insurance is not foolish. The FDIC says monitoring bank solvency requires fixed costs and expertise that cannot be expected of small depositors, and that deposit insurance reduces the risks created when a bank run forces a rushed sale or spreads stress to similarly situated banks[s]. The problem begins when the guarantee is treated as a substitute for discipline. The public notices danger when the story looks like financial bubbles, but the quieter version is a balance sheet that learns somebody else will absorb enough pain to keep the system standing.

The FDIC’s own answer is not to abandon protection. It says regulation and supervision are essential for helping deposit insurance meet its objectives and constrain moral hazard[s]. That is the correct frame. A safety net without supervision is not compassion. It is a training program for risk.

The Subsidy Bill Is The Behavior Map

Perverse incentives become hardest to defend when the public sees their scale. The World Bank reported that direct government expenditures on agriculture, fishing, and fossil fuel subsidies total $1.25 trillion a year[s]. That figure is not a footnote to policy. It is a map of what governments make cheaper.

The same World Bank release says fisheries subsidies exceed $35 billion each year and are a key driver of dwindling fish stocks, oversized fishing fleets, and falling profitability[s]. That sentence contains the whole pathology. Public money keeps capacity alive after the resource base is already strained, then policy makers wonder why the strain persists.

The IMF’s roughly $7.4 trillion 2024 estimate makes the larger point. It says explicit subsidies are fiscal subsidies, while implicit subsidies primarily reflect underpricing of environmental costs[s]. Perverse incentives thrive in that gap between the immediate receipt and the delayed invoice.

The Counterargument Deserves Respect

A serious defense of these programs starts with the word “shock.” When prices, floods, or financial stress hit, governments are expected to keep households alive, payments moving, and communities intact. Any argument that ignores those duties is not tough-minded. It is performative.

The World Bank’s own reform guidance reflects that reality. It says successful subsidy reform must compensate the most vulnerable groups through social assistance programs, such as cash transfers[s]. The humane answer is not to rip away protection and call the pain honesty. The humane answer is to protect people without protecting the behavior that keeps producing the emergency.

That distinction is where governments often fail. They subsidize the fuel instead of the household. They subsidize rebuilding instead of mitigation. They guarantee stability without charging enough for fragility. Then the perverse incentives become politically invisible because each beneficiary can describe a real need.

How To Stop Paying For The Wrong Thing

Reform should begin with a brutal question: what behavior does this payment reward? If the answer is more exposure, more pollution, more leverage, or more depletion, then the program needs a redesign even if its stated purpose is noble.

One rule is to make support portable to people, not permanently attached to harmful consumption. Help vulnerable households through cash or targeted rebates, while letting the risky activity face a price closer to its real cost. Another rule is to pay for risk reduction before paying for repeated rescue. A flood program that rewards elevation, relocation, and mitigation teaches a different lesson than one that mainly socializes repeated loss.

A third rule is independent review with teeth. A useful borrowing from judicial gatekeeping is the insistence that official expertise should be tested against evidence, not accepted because it arrives on government letterhead. Budgets deserve the same discipline: if a subsidy survives only because its costs are delayed or hidden, it should not survive unchanged.

Perverse incentives persist because they are politically convenient. They let officials appear generous without asking who pays later. They let voters receive a benefit without seeing the full bill. They let industries call public support a bridge long after it has become a business model.

The cure is not cruelty. It is alignment. If governments want less risk, they should stop discounting risk. If they want less pollution, they should stop making pollution artificially cheap. If they want stable finance, they should pair protection with supervision strong enough to make the guarantee honest. The public should judge a policy less by the virtue of its stated goal than by the behavior it rewards.